2023 Mid-Year Event - Recap

/On July 27th, 2023, Gilbert & Cook hosted a mid-year update event, hosting an interactive panelist discussion on financial headlines in the news. Our panel included Chris Cook, CPA, CFA, Chief Investment Strategist, Megan Rosenstiel, CFP®, CDFA®, AWMA®, ADPA®, LTCP, Director of Advisory Services, and Zach Ripka, CFP®, CPA/PFS, CEPA, Planning & Tax Strategist. Let’s take a look back at some of the topics that have been hitting the headlines.

As discussed by our panelists, Megan Rosenstiel,and Zach Ripka, the sweeping legislation of the SECURE ACT 2.0 has dozens of significant provisions. These updated rules can seem cumbersome and you want to know and understand how these affect you.

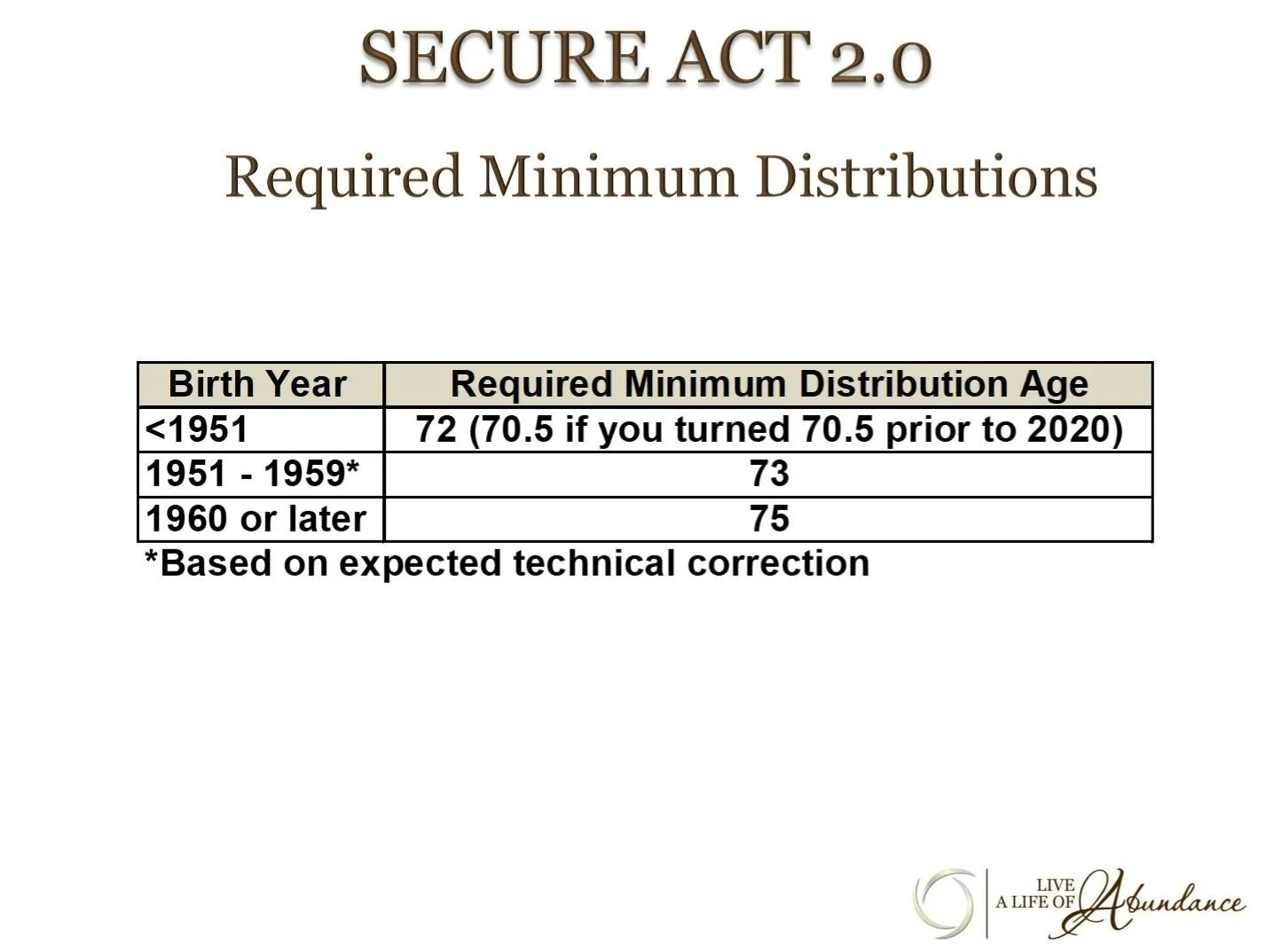

First and foremost: Required Minimum Distributions

One of the most critical changes was the increase in the age at which owners of various retirement accounts MUST begin taking required minimum distributions (RMDs). Starting in 2033, RMDs must begin at age 75. If you turned age 72 before January 1, 2023, you must continue taking distributions under the prior rules. But if you are turning 72 in 2023 and have already scheduled your withdrawal, we may want to revisit your plan.

Zach went on to share how there have been revisions to the rules surrounding Roth accounts. Starting in 2024, pending certain conditions, individuals can roll a 529 Education Savings Plan into a Roth IRA. If a child receives a scholarship, goes to a less expensive school, or doesn't go to school, the money can be repositioned into a retirement account.

Individuals will be able to roll over up to a total of $35,000 from 529 plans to a Roth IRA for the same beneficiary, provided 529 accounts have been held for at least 15 years. The annual rollover amounts will be subject to the annual Roth IRA contribution limit, but not the Roth IRA income limits. Any contributions to a 529 plan within the last 5 years (and the earnings on those contributions) are ineligible to be moved to a Roth IRA.

The new legislation aligns the rules for Roth 401(k)s and Roth 403(b)s with Roth Individual Retirement Account (IRA) rules. This means that starting in 2024, there is no longer a required minimum distribution from Roth accounts in employer retirement plans.

As it should be noted, previously, employer matching contributions were required to be deposited into each employee’s pre-tax account in the retirement plan. The new legislation allows employer matches to the Roth portion of the account for electing employees. However, this now makes any Roth Employer Match, taxable income to the employee.

Lastly, Zach went over some additional highlights that many found helpful. The maximum Qualified Charitable Distributions (QCDs) amount will start indexing for inflation in 2024. Currently, the maximum QCD amount is $100,000 per taxpayer. The limit applies on an individual basis, so for a married couple, each person who is at least 70½ years old can make a QCD as long as it remains under the limit (currently $100,000 per taxpayer per year). Individuals will also be able to make a one-time distribution of up to $50,000 to a charitable remainder trust or charitable gift annuity.

Our final panelist, Chris Cook, CPA, CFA, Chief Investment Strategist, gave us some insight into the current market while debunking some current headlines.

Headline: Worst Inflation in 20 Years

Reality: On a 4-yr rolling average, inflation is higher than we are used to, but not out of bounds from where we have been the last 30 years. What it is not, currently, is 1981, where the rolling, 4-year average inflation rate was nearly 11%. Inflation continues to cool and will eventually reach longer term trend levels.

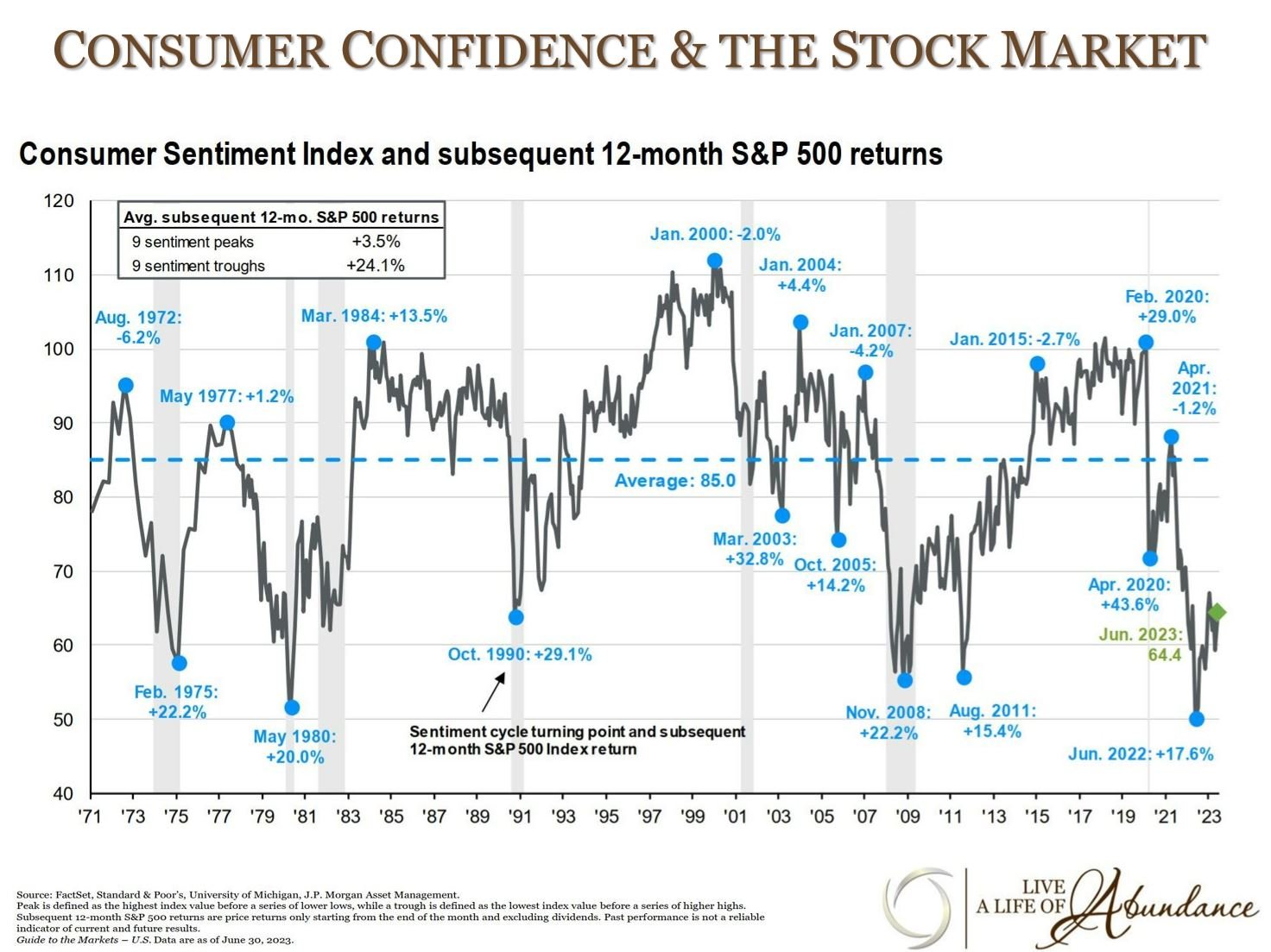

In June of 2022, the Index reached the lowest point in over 50 years, indicating extreme consumer pessimism i.e. people just didn't feel good about things. However, in terms of economic data, this was not that bad of times. The unemployment rate was low, around 3.7%, and while interest rates were higher, they weren't as high as other inflationary periods in history. These low points typically represent opportunities for investors especially when economic data is positive or not as bad as we are being lead to believe in the news. Fast forward to today, with a strong stock market recovery, the outcome over the last 12 months has been consistent with previous sentiment bottoms. This is yet another reminder to stay the course as a long-term investor. The Gilbert & Cook Investment Team is constantly positioning portfolios for these opportunities and is ready to act when they arise.

Disclosure: The presentation on July 27th, 2023, was meant for informational purposes only. Services offered through Gilbert & Cook, Inc. a Registered Investment Adviser. Please note we cannot accept any type of market orders requested via email or voicemail. Advisory services are only offered to clients or prospective clients where Gilbert & Cook, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Gilbert & Cook, Inc. unless a client service agreement is in place. Gilbert & Cook, Inc. does not offer tax or legal advice. Consult with an attorney for legal advice and a qualified tax professional for tax advice.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark, the CERTIFIED FINANCIAL PLANNER™ certification mark, and the CFP® certification mark (with plaque design) logo in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.