2022 Year in Review

/2022 was definitely a year that we won’t soon forget. Through it all, we have plenty to celebrate. Here are some highlights from your Gilbert & Cook team!

2022 was definitely a year that we won’t soon forget. Through it all, we have plenty to celebrate. Here are some highlights from your Gilbert & Cook team!

In the final days of 2022, Congress passed a new set of rules designed to make it easier to contribute to retirement plans and access those funds earmarked for retirement.

SECURE 2.0 builds upon its predecessor, the Setting Every Community Up for Retirement Enhancement (SECURE) Act, which was passed in 2019.

The sweeping legislation has dozens of significant provisions. To help see what changes may affect you, the major provisions of the new law are broken down into four sections below.

The RMD age will rise to 73 in 2023. By far, one of the most critical changes was increasing the age at which owners of various retirement accounts MUST begin taking required minimum distributions (RMDs). Starting in 2033, RMDs must begin at age 75. If you turned age 72 before January 1, 2023, you must continue taking distributions under the prior rules. But if you are turning 72 in 2023 and have already scheduled your withdrawal, we may want to revisit your plan.1

Reduction in the RMD Excise Tax. Previously a 50% excise tax was imposed if you missed taking an RMD by the deadline. Starting in 2023, if you miss an RMD for any reason, the penalty tax drops to 25%. If you fix the mistake promptly, the penalty may drop to 10%.2

401(k) and Employer-sponsored Plan Catch-Up Contributions. Starting January 1, 2025, employees aged 60 through 63 can make catch-up contributions equal to the greater of $10,000 (indexed annually for inflation) or 150% of the regular catch-up limit to workplace retirement plans. Also, the catch-up amount for people aged 50 and older in 2023 has increased to $7,500. However, beginning in 2024, all catch-up contributions for those earning more than $145,000 in a particular year will have to be (taxable) Roth contributions.3

Traditional and Roth Catch-Up Contributions. Currently, individuals aged 50 or older can make an additional catch-up contribution to a Traditional or Roth IRA up to $1,000 per year. In 2024, the $1,000 amount will be indexed for inflation on an annual basis.

Automatic Enrollment. Beginning in 2025, the Act requires employers in newly-established plans to enroll employees into workplace plans automatically at a 3% contribution rate. The contribution rate automatically increases by 1% per year until the employee is contributing at least 10%. However, employees can choose to opt-out.4

Student Loan Matching. In 2024, companies can match employees’ student loan payments with retirement contributions. The rule change offers workers an opportunity to receive employer-funded retirement plan contributions while paying off their student loans.5

529 to a Roth. Starting in 2024, pending certain conditions, individuals can roll a 529 education savings plan into a Roth IRA. If your child gets a scholarship, goes to a less expensive school, or doesn't go to school, the money can get repositioned into a retirement account. Individuals will be able to roll over up to a total of $35,000 from 529 plans to a Roth IRA for the same beneficiary, provided 529 accounts have been held for at least 15 years. The annual rollover amounts will be subject to the annual Roth IRA contribution limit, but not the Roth IRA income limits. Any contributions to a 529 plan within the last 5 years (and the earnings on those contributions) are ineligible to be moved a Roth IRA.6

SIMPLE and SEP. From 2023 onward, employers can make Roth contributions to Savings Incentive Match Plans for Employees or Simplified Employee Pensions.7

Employer Matching Roth Contributions. Previously, employer matching contributions were required to be deposited into each employee’s pre-tax account in the retirement plan. The new legislation allows employer matches to the Roth portion of the account for electing employees. Note, however, that electing a Roth match will subject the employee to taxation on the matching amount contributed to the plan by the employer.

Roth 401(k)s and Roth 403(b)s. The new legislation aligns the rules for Roth 401(k)s and Roth 403(b)s with Roth Individual Retirement Account (IRA) rules. Effective January 1, 2024, the legislation no longer requires minimum distributions from Roth Accounts in employer retirement plans.8

Support for Small Businesses. Beginning January 1, 2023, the new law will increase the credit to help defray the administrative costs of setting up a retirement plan. The credit increases to 100% (from 50%) for businesses with less than 50 employees. By boosting this credit, lawmakers hope to remove one of the most significant barriers to small businesses offering a workplace plan.9

Qualified Charitable Donations (QCD). From 2023 onward, QCD donations will adjust for inflation. The limit applies on an individual basis, so for a married couple, each person who is at least 70½ years old can make a QCD as long as it remains under the limit (currently $100,000 per taxpayer per year).9 Individuals will also be able to make a one-time distribution of up to $50,000 to a charitable remainder trust or charitable gift annuity. 10

New Exceptions to the 10% early-withdrawal penalty. Generally, distributions from a retirement savings account before age 59½ are subject to an early withdrawal penalty unless an exception applies. The new legislation provides several new exceptions to the penalty, including terminal illness, domestic abuse, payment of long-term care insurance premiums, to recover from a federally declared disaster area, and an emergency personal expense.

Retirement Savings Lost and Found. The Act intends to establish a searchable database for lost 401(k) plan accounts within two years of the legislation’s enactment.

Saver’s Credit transitioning to a Saver’s Match. Currently, low- and moderate-income taxpayers receive a credit up to $1,000 for retirement savings. Starting in 2027, the credit transitions into a match that will be contributed to the individual’s retirement account.

There are several additional provisions in the new SECURE Act 2.0 legislation. A few examples include providing credits for enrolling military spouses immediately in employer plans, expansion of lifetime income products in retirement plans, improved retirement plan coverage for part-time workers, S-Corporation ESOP opportunities, and several other provisions.

The provisions listed above summarize only a portion of the Secure Act 2.0. The Gilbert & Cook Team looks forward to analyzing the impact the changes have on your financial situation to best understand how to assist you in Living a Life of Abundance.

Also, retirement rules can change without notice, and there is no guarantee that the treatment of specific rules will remain the same. This article intends to give you a broad overview of SECURE 2.0. It is not intended as a substitute for real-life advice. If changes are appropriate, we will outline an approach and work with your tax and legal professionals, if applicable.

Sincerely,

Gilbert & Cook Team

The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced to provide information on a topic that may be of interest. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.Citations:1. Fidelity.com, December 23, 20222. Fidelity.com, December 22, 20223. Fidelity.com, December 22, 20224. Paychex.com, December 30, 20225. PlanSponsor.com, December 27, 20226. CNBC.com, December 23, 20227. Forbes.com, January 5, 20238. Forbes.com, January 5, 20239. Paychex.com, December 30, 202210. FidelityCharitable.org, December 29, 2022By Reece Oleson, CFP®, RICP®, CEPA

Director of Financial Planning

Life Insurance is an important financial planning tool. Life Insurance benefits can be designed to meet many goals, such as replacing income, paying off debts, or fully funding college. Let’s talk about three common misconceptions about Life Insurance:

1. I don’t need Life Insurance.

If your spouse or children’s lifestyle today or in the future would be negatively impacted without your income, Life Insurance can provide additional assets to support their lifestyle.

2. Life Insurance is expensive.

Term insurance is very cost-efficient. For example:

A 20-year term policy with a $1,000,000 death benefit for a 40 year old man at standard rates is about $100/month.*

A 20-year term policy with a $1,000,000 death benefit for a 40 year old woman at standard rates is about $80/month.*

At standard plus, preferred, or preferred plus rates, premiums are even cheaper!

3. I already have Life Insurance through work, so that should be enough.

Life insurance through employers is a good start, especially when you are younger, but isn’t generally enough to replace the insured’s income. Most employers only provide around $50,000 to 1 year’s salary of life insurance at no cost.

Many employers do allow you to purchase additional coverage, and it may be easy to purchase as it often does not require underwriting. It is likely more expensive than term life purchased on your own, especially for older workers as most premiums increase as you age, and you may not be able to get enough coverage to meet your needs.

Term life insurance is generally the most affordable life insurance option. It provides coverage when you need it and goes away when you no longer need it.

The money you save by purchasing term insurance can be used toward your other goals, whether that is a purchase for today or saving for tomorrow!

Contact Gilbert and Cook to analyze your life insurance needs & provide cost-efficient options to meet those needs.

*Source: TNBC term life insurance quotes for Iowa resident, 11/16/2022.

"I am thrilled to be joining the private wealth management firm of Gilbert & Cook where we are committed to helping people live more meaningful and fulfilling lives. We employ a process to crystalize goals, provide clarity, and instill confidence with our clients to help them to Live a Life of Abundance. At Gilbert and Cook, it’s more than just the numbers, it’s about living your best life." - Wendy

Wendy Stenberg joined Gilbert & Cook as an Advisor in November 2022. With over thirty years of experience, Wendy is a dedicated and experienced wealth management professional who is passionate about exceeding client expectations and building long-term meaningful relationships to help clients achieve personal goals and aspirations.

In her new role, Wendy works in collaboration with other members of the Gilbert & Cook team to provide sophisticated strategies and service to her clients. Gilbert & Cook is thrilled and honored to welcome Wendy to the team. We are delighted that she has decided to lend her talents and experience to inspire abundance with our clients and Gilbert & Cook family.

Welcome Wendy!

In today's world where everything is digital, how can you keep your data protected? We took a further look into this topic to provide clear solutions.

On September 16th 2022, Gilbert & Cook hosted a cybersecurity event, featuring three members of our Compliance Committee. We presented the ways Gilbert & Cook protects your data, the ways Charles Schwab protects your data, and ways you can protect your data.

Here are the big takeaways from the event:

Be password smart; create a strong password by using letters, symbols, and numbers. Never use the same password for multiple logins. For critical accounts such as your bank account, credit cards, retirement account, and phone, setup two-factor authentication. Two-factor authentication is where you are required to enter a generated code sent to you as a text message or email to gain access to your account.

Think before you click on links in an email or text. You can do this by hovering your cursor over any URL links being sent; is the URL link a legitimate site? Scammers will attempt to disguise themselves as someone familiar to you, verify the sender's email address or phone number. Another area to look at is the time the email or text was sent. Often times scammers will send emails or texts outside of regular business or daily hours.

Keep your devices updated. Computer and mobile operating systems offer updates that will include security patches. These patches are important as they allow your devices to be up-to-date on the most recent systems upgrades. Typically these updates are pushed out to you, and you are prompted to allow them to update and install.

Almost everyone has home Wi-Fi, password protect yours. Ensure your network is private, check to make sure only your devices are using your internet. Do not use public Wi-Fi networks such as those available at the grocery store, library, coffee shop, or airport. When you need to use Wi-Fi while on-the-go, use your phone as a hotspot.

Disclosure: The presentation on September 16th 2022 was meant for informational purposes only. The featured speaker is not affiliated with Gilbert & Cook, Inc. Gilbert & Cook, Inc. does not offer tax or legal advice. You should consult with an attorney for legal advice and a qualified tax professional for tax advice. Gilbert & Cook, Inc. is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Gilbert & Cook, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Gilbert & Cook, Inc. unless a client services agreement is in place.

On June 30th 2022, Gilbert & Cook hosted a mid-year update event, featuring BlackRock economist, Mark Peterson. Halfway through the year and it's certainly been a remarkable historic start. Let’s take a look back at some of the unusual outcomes thus far.

1) We’ve clearly seen a challenging start for both stocks and bonds so far in 2022. Stocks and bonds are both negative; which is very rare. Over the last 95 years, stocks and bonds have been negative at the same time in the same calendar year, twice – in 1931 and 1969. The culprit? The market trying to digest the economy and figure out where we’re headed from here. This year, the markets priced in a lot of short-term interest rate increases by the federal reserve in effort to slow the economy and bring inflation back to more modest levels.

2) Speaking of inflation… 2022 saw the worst start ever for bonds going back to 1926, down more than 10%. However, we’ve reset interest rates and bond returns to much healthier levels for investors going forward.

3) Looking at the stock side…through the end of June we saw the 5th worst start for stocks, out of 95 calendar years. However, history tells us that the first half of the year and the second half of the year are not correlated. In fact, in 7 out of the 9 worst starts to the calendar year, stocks have ended up much higher 12 months later.

4) A big part of the story on the stock side is the volatility. If we look at the number of days that the market moved up or down by more than 2%; as of June 30th, 2022 has seen 14 down days and 12 up days, greater than 2%. Interestingly enough, the best and worst days in market history are often around the corner from each other. For example, in March of 2020 we had 3 of the worst days in stock market history – but we also had 5 of the best days in market history in the same month. Diversification is more important than ever and it’s important to remember that when we see volatility in the market, don’t let it derail your long-term financial plans.

5) Consumer satisfaction level is often a contrarian indicator for the market. History shows that if less than a 3rd of the country is satisfied, 1 year later stocks are up better than 15% on average. The opposite is true as well; whenever there is a lot of satisfaction, expectations are high and returns are lower.

Disclosure: The presentation on June 30th 2022 was meant for informational purposes only. The featured speaker is not affiliated with Gilbert & Cook, Inc. Gilbert & Cook, Inc. does not offer tax or legal advice. You should consult with an attorney for legal advice and a qualified tax professional for tax advice. Gilbert & Cook, Inc. is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Gilbert & Cook, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Gilbert & Cook, Inc. unless a client services agreement is in place.

Sources: Morningstar as of 6/30/22. U.S. bonds represented by the IA SBBI US Gov IT Index from 1/1/26 to 1/3/89 and the Bloomberg U.S. Agg Bond TR Index from 1/3/89 to 6/30/22. U.S. stocks are represented by the S&P 500 Index from 3/4/57 to 6/30/22 and the IA SBBI U.S. Lrg Stock Tr USD Index from 1/1/26 to 3/4/57, unmanaged indexes that are generally considered representative of the U.S. stock market during each given time period. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index

This event is meant for informational purposes only. The featured speaker is not affiliated with Gilbert & Cook, Inc. Gilbert & Cook, Inc. does not offer tax or legal advice. You should consult with an attorney for legal advice and a qualified tax professional for tax advice. Gilbert & Cook, Inc. is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Gilbert & Cook, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Gilbert & Cook, Inc. unless a client services agreement is in place.

Amy joined Gilbert &Cook, Inc. a year ago as our Director of Operations.

An organization that is near and dear to Amy, is Dobbers Up . The organization was created in 2007 to help support Dan Dowson & his family during his courageous battle with ALS. Dan lost his battle in 2009 but never lost his faith, humor, or giving spirit. Amy has been part of Dobbers Up since it's inception in 2007. She serves as a Board Member & Treasurer. Amy, along with several other volunteers, spend countless hours fundraising, organizing, and participating in the annual Dobbers Up Golf Tournament.

Amy believes the spirit & focused mission of Dobbers Up brings out the good in people, while providing support to families that have been "thrown a curveball in life".

On June 10th, Gilbert & Cook supported the 15th annual golf tournament for Dobbers Up. Since 2009, Dobbers Up has made contributions to local families who have been "thrown a curveball in life", totaling more than $100,000.

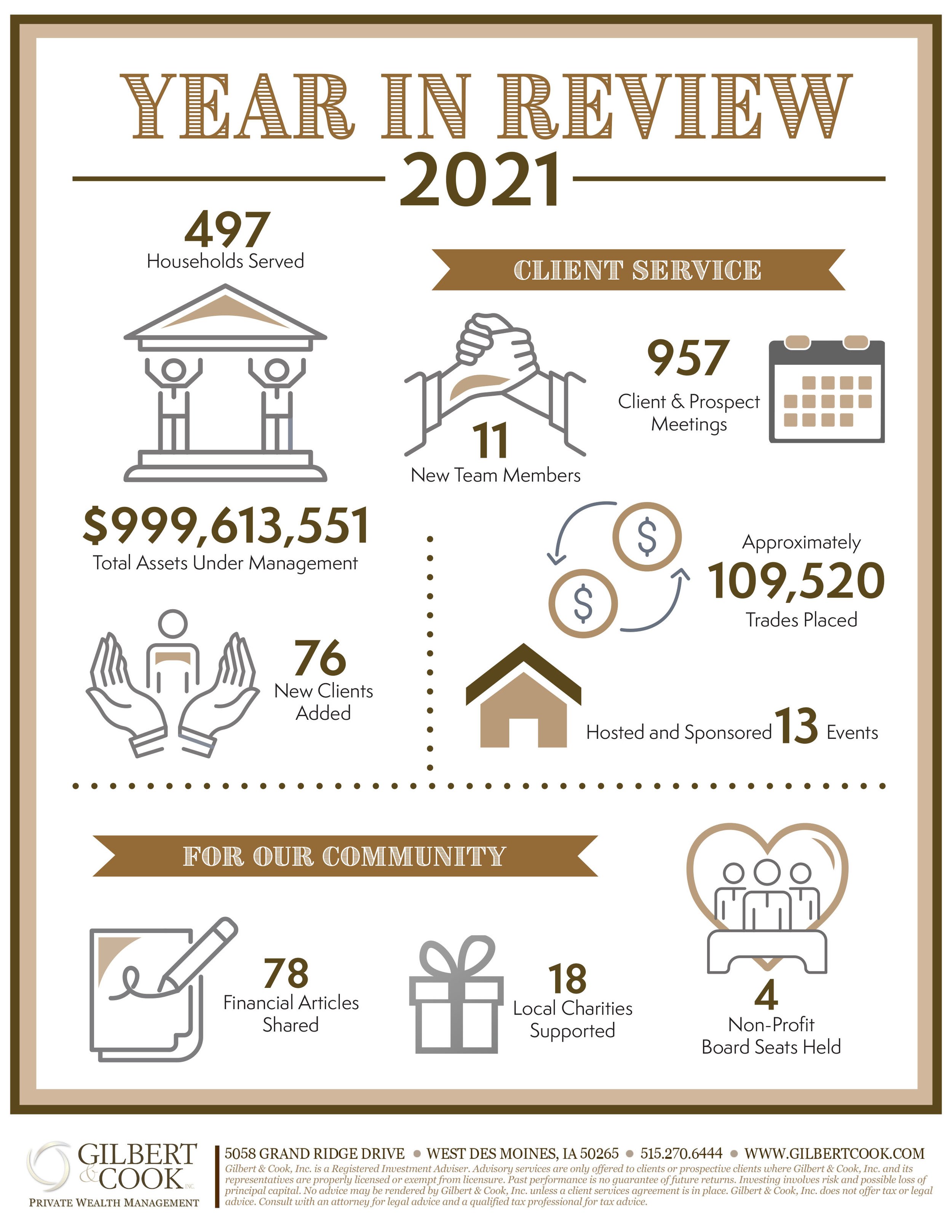

What a year! Here’s a look back at what we’ve been up to at Gilbert & Cook.

CityWire RIA has selected the fastest-growing firms in every state based on the previous years Form ADV data reported to the Securities and Exchange Commission at the time of publication. Read more about this honor on citywireusa.com

The end of the year can help remind us of last-minute things we need to address and the goals we want to pursue. To that end, here are some aspects of your financial life to think about as this year leads into the next.

Keep in mind, this article is for informational purposes only. Make certain to contact a tax or legal professional before modifying your tax strategy.

Set a goal to review your investments with your Advisor at your next meeting. Your Gilbert & Cook investment team will review your portfolio positions and asset allocation. Remember, asset allocation and diversification are approaches to help manage investment risk. They do not guarantee against investment loss.

You may want to consider contributing the maximum to your retirement accounts. It’s also a good idea to review any retirement accounts you may have through your work. This is also a great time to decide on making catch-up contributions if you are eligible.

$19,500 for 401(k), 403(b), 457 (b) Roth 401(k); $6,500 catch-up provision for individuals 50 and over

$13,500 SIMPLE plans; $3,000 catch-up contribution for individuals 50 and over

$6,000 Roth IRA / IRA contribution; $1,000 catch-up contribution for individuals 50 and over

Consider checking in with your tax or legal professional before the year ends, especially if you have questions about an expense or deduction from this year. Also, it may be a good idea to review any sales of property as well as both realized and unrealized losses and gains. (1)

Beginning in 2023 you will no longer be able to deduct your Federal Taxes paid from your Iowa State Tax Return. At the corporate level the Federal deduction gets eliminated starting in 2022. To take advantage of the allowable deduction on your 2021 tax return, please be sure to pay all federal tax estimates in 2021 as opposed to waiting until January of 2022 when estimates are due.

Plan charitable contributions or contributions to education accounts and make any desired cash gifts to family members. The annual federal gift tax exclusion allows you to give away up to $15,000 in 2021, meaning you can gift as much as $15,000 to as many individuals as you like this year. Such gifts do not count against the lifetime estate tax exemption amount, as long as they stay beneath the annual federal gift tax exclusion threshold. Besides outright gifts, you can explore creating and funding trusts on behalf of your family. The end of the year is also a good time to review any trusts you have in place. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations. (1,2)

Note: If you are making Qualified Charitable Distributions (QCDs), make sure that you communicate that to your CPA so that it is reported on your taxes.

The end of the year is an excellent time to double-check that your policies and beneficiaries are up to date. Don’t forget to review premium costs and beneficiaries and think about whether your insurance needs have changed. Several factors could impact the cost and availability of life insurance, such as age, health, and the type of insurance purchased, as well as the amount purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, you may pay surrender charges, which could have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Finally, don’t forget that any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Here are some questions to ask yourself when evaluating any large life changes in the last year:

Did you happen to get married or divorced this year?

Did you move or change jobs?

Did you buy a home or business?

Was there a new addition to your family this year?

Did you receive an inheritance or a gift?

All these circumstances can have a financial impact on your life as well as the way you invest and plan for retirement and wind down your career or business.

As always, your Gilbert & Cook team is here for you. Please talk to your Advisor if you have any questions regarding your financial situation.

Citations

1. turbotax.intuit.com, October 16, 2021

2. irs.gov, October 14, 2021

From Charles Schwab Advisor Services:

Cybercrime and fraud are serious threats and constant vigilance is key. While my firm plays an important role in helping protect your assets, you can also take action to protect yourself and help secure your information. This checklist summarizes common cyber fraud tactics, along with tips and best practices. Many suggestions may be things you’re doing now, while others may be new. We also cover actions to take if you suspect that your personal information has been compromised. If you have questions, we’re here to help.

Cyber criminals exploit our increasing reliance on technology. Methods used to compromise a victim’s identity or login credentials – such as malware, phishing, and social engineering – are increasingly sophisticated and difficult to spot. A fraudster’s goal is to obtain information to access to your account and assets or sell your information for this purpose. Fortunately, criminals often take the path of least resistance. Following best practices and applying caution when sharing information or executing transactions makes a big difference.

Safe practices for communicating with our firm:

Keep us informed regarding changes to your personal information.

Expect us to call you to confirm email requests to move money, trade, or change account information.

Establish a verbal password with our firm to confirm your identity, or request a video chat.

Schwab takes your security seriously and leverages protocols and policies to help protect your financial assets. Below are actions you can take to reinforce their efforts and resources to assist you in keeping your account safe:

Confirm your identity using Schwab’s voice ID service when calling the Schwab Alliance team for support.

Use two-factor authentication, which requires you to enter a unique code each time you access your Schwab accounts.

Review the Schwab Security Guarantee, which covers 100% of any losses in any of your Schwab accounts due to unauthorized activity.

To learn more, visit Schwab’s Client Learning Center.

Be aware of suspicious phone calls, emails, and texts asking you to send money or disclose personal information. If a service rep calls you, hang up and call back using a known phone number.

Never share sensitive information or conduct business via email, as accounts are often compromised.

Beware of phishing and malicious links. Urgent-sounding, legitimate-looking emails are intended to tempt you to accidentally disclose personal information or install malware.

Don’t open links or attachments from unknown sources. Enter the web address in your browser.

Check your email and account statements regularly for suspicious activity.

Never enter confidential information in public areas. Assume someone is always watching.

Leverage our electronic authorization tool to verify requests. Featuring built-in safeguards, this is the fastest and most secure way to move money.

Review and verbally confirm all disbursement request details thoroughly before providing your approval, especially when sending funds to another country. Never trust wire instructions received via email.

Don’t use personal information as part of your login ID or password and don’t share login credentials.

Create a unique, complex password for each website, Change it every six months. Consider using a password manager to simplify this process.

Keep your web browser, operating system, antivirus, and anti-spyware updated, and activate the firewall.

Do not use free/found USB devices. They may be infected with malware.

Check security settings on your applications and web browser. Make sure they’re strong.

Turn off Bluetooth when it’s not needed.

Dispose of old hardware safely by performing a factory reset or removing and destroying all storage data devices.

Be cautious when accepting “friend” requests on social media, liking posts, or following links.

Limit sharing information on social media sites. Assume fraudsters can see everything, even if you have safeguards.

Do not visit websites you don’t know, (e.g., advertised on pop-up ads and banners).

Log out completely to terminate access when exiting all websites.

Don’t use public computers or free Wi-Fi. Use a personal Wi-Fi hotspot or a Virtual Private Network (VPN).

Hover over questionable links to reveal the URL before clicking. Secure websites start with “https,” not “http.”

Call your Advisor or service team so that they can watch for suspicious activity on your accounts and collaborate with you on other steps to take.

Visit these sites for more information and best practices:

StaySafeOnline.org: Review the STOP. THINK. CONNECT™ cybersecurity educational campaign.

OnGuardOnline.gov: Focused on online security for kids, it includes a blog on current cyber trends.

FBI Scams and Safety provides additional tips, https://www.fbi.gov/scams-and-safety

On Wednesday, July 14th 2021, Gilbert & Cook Private Wealth Management welcomed guests to a timely discussion on the economy and recent updates in various financial planning topics and considerations. Gilbert & Cook Founder & Advisor, Linda Cook, moderates a panel of professionals as they discuss the 2021 economic outlook, the current state of the market and current event topics and considerations within the financial planning industry.

Answered by Gilbert & Cook's Chief Investment Strategist, Chris Cook, CPA, CFA

Answered by Gilbert & Cook's Chief Investment Strategist, Chris Cook, CPA, CFA

Answered by Gilbert & Cook’s Chief Investment Strategist, Chris Cook, CPA, CFA

Answered by Gilbert & Cook's Chief Investment Officer, Brandon Grimm, MBA, CFA.

Answered by Gilbert & Cook’s Chief Investment Strategist, Chris Cook, CPA, CFA

Disclosure: This event is meant for informational purposes only. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Gilbert & Cook, Inc. does not offer tax or legal advice. You should consult with an attorney for legal advice and a qualified tax professional for tax advice. Gilbert & Cook, Inc. is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Gilbert & Cook, Inc. and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Gilbert & Cook, Inc. unless a client services agreement is in place.

No one knows your business like you do. However, there are elements to running a successful business, that have little to do with the core business you’re managing - but are still critically important to your overall long-term success.

Your company retirement plan is a perfect example.

You know you need excellent benefits in order to attract, reward and retain exceptional employees. You know that you need to keep these benefits costs reasonable and under control. You also know that you don’t want the complexities of monitoring this program taking up your valuable work time.

The Gilbert & Cook team has developed a comprehensive process, built around bringing clarity to the many choices you face and providing you with confidence in making financial decisions for your business and the individuals and families you support.

Led by Retirement Advisors, Jerit Tripp & Jarret Sheets, Gilbert & Cook’s Retirement Plan Services provide businesses with customized suite of services to contribute to the success of your company’s retirement plan.

Contact a Gilbert & Cook Advisor today, to get a complimentary Second Opinion on your situation.

Recently, the Internal Revenue Service (I.R.S.) announced that tax season will start a little later than usual. This year the I.R.S. will begin accepting and processing 2020 individual tax returns on Friday, February 12, 2021. (1)

In light of the December 27 tax law changes which brought a second round of Economic Impact Payments and other benefits to many, the I.R.S. will use this additional time to update, program, and test their systems. (1)

However, if you intend to work with a tax professional or use tax software, there's no need to wait. If you prepare your return now, not only will you have your taxes done and out of the way, but your filings can be transmitted to the I.R.S. starting February 12. (1)

Even with this new date in mind, your deadline to file is still April 15. To request an extension, make sure you do so by April 15. This may grant you until October 15 to file your 2020 tax returns. However, this is an extension for filing only. The I.R.S. still requires you to pay any taxes due by the original filing date of April 15. (1)

Filing one’s tax returns can be a complicated and sometimes daunting process. If you have questions regarding your personal situation, please consult your CPA or a licensed tax professional.

Want More? Click here to download a “2021 Tax Guide” to help prepare for the upcoming tax season.

1 - IRS.gov, January 15, 2021

Disclosure: Gilbert & Cook, Inc. does not provide tax or legal advice. For advice regarding your individual tax situation please consult with a licensed tax professional.

Economic Update - written January 25th 2021

Ready… Set… Go!

The stock market’s first hurdle of the New Year was to assess the runoff elections happening for the two Senate seats in Georgia. A special election such as this has only happened a handful of other times in our nation’s history, so the market appeared anxious about the process.

The market’s second hurdle was the electoral college count that would confirm Joe Biden as the 46th president of the United States. A protest during the vote count unnerved investors, and most of the New Year’s rally was undone. However, just one day later the market climbed higher as traders looked past the unrest.

Stocks Scale New Heights

Midway into the 1st month of the new year stocks rallied. Testimony from incoming Treasury Secretary Janet Yellen raised hopes for a new round of federal spending when she suggested to the Senate Finance Committee that lawmakers should “act big” on fiscal stimulus.

An orderly presidential transition and the anticipation of a more effective vaccine distribution plan contributed to stocks touching multiple new highs this month. Investor enthusiasm was further supported by a strong start to the fourth-quarter earnings season.

What does this fast-paced market activity mean for investors?

There will always be a lot of noise. But remember, making a change to your portfolio should be driven by sound analysis and preparation. Reacting impulsively to market volatility can compromise the return of your portfolio and your overall financial plan. As Advisors we have come to expect the volatility that comes along with investing and have anticipated these trends as we developed your overall financial strategy.

If you have any questions about your personal financial situation, please reach out to a member of your Gilbert & Cook Abundance Team.

YEAR-END ECONOMIC STIMULUS BILL

On Monday, December 21st, congress passed legislation which offers a wide range of help, both for individuals and for struggling elements of the economy - including direct payments, enhanced unemployment benefits and tax breaks. Here are a few highlights of what’s inside the massive year-end compromise:

$166 billion in direct checks - Individuals making up to $75,000 a year will receive a payment of $600, while couples making up to $150,000 will receive $1,200, in addition to $600 per child.

$120 billion in extra unemployment help - Jobless workers will get an extra $300 per week in federal cash through March 14.

$325 billion small business boost - Pandemic-ravaged small businesses would see a total of $325 billion, including $284 billion in loans through the Paycheck Protection Program, $20 billion for businesses in low-income communities and $15 billion for struggling live venues, movie theaters and museums.

Tax Benefits - The legislation allows businesses to deduct expenses associated with their forgiven PPP loans, in addition to expanding the employee retention credit intended to prevent layoffs. The package rolls over a variety of temporary tax breaks known as “extenders” - some for multiple years. It also extends a payroll tax subsidy for employers offering workers paid sick leave and boosts the Earned Income Tax Credit.

WALL STREET

Stocks climbed higher amid the COVID-19 vaccine rollout and an improving outlook after a fiscal stimulus bill.

The Dow Jones Industrial Average, which has lagged all year, gained 0.44%. The Standard & Poor’s 500 picked up 1.25% while the Nasdaq Composite index surged 3.05%. The MSCI EAFE index, which tracks developed overseas stock markets, rose 2.44%. (1,2,3)

STOCKS CLIMB HIGHER

In a week that celebrated the national rollout of a COVID-19 vaccine, market enthusiasm was tempered by worries of infection caseload and fresh economic lockdowns.

Investors turned their focus to the fiscal stimulus negotiations in Washington, D.C., with the hope that a relief bill may be the bridge that gets the economy over its near-term troubles until vaccine distribution grows more widespread.

These negotiations were not smooth sailing. When a compromise bill appeared to gather support, markets quickly moved higher, with the Dow Jones Industrial Average, S&P 500, and NASDAQ Composite all setting new record high closes on Thursday. (4) Stocks slipped in the final day of trading as stimulus hopes wavered.

FED OUTLOOK ON THE ECONOMY IMPROVES

The Federal Reserve on Wednesday concluded its last meeting of the Federal Open Market Committee for 2020. Fed officials provided more detail for its monthly bond purchase program and reiterated their commitment to a monthly purchase of $120 billion of Treasury and mortgage-back securities until its inflation and employment goals are met. (5)

The Federal Reserve also raised its outlook on the U.S. economy. It revised its September forecast of a 3.7% decline in GDP in 2020 to a 2.4% decline, and increased its 2021 GDP growth forecast from 4.0% to 4.2%. It also expects unemployment at 2020 year-end would fall to 6.7%, substantially lower than its earlier estimate of 7.6%. (6)

CITATIONS:

1. The Wall Street Journal, December 18, 2020

2. The Wall Street Journal, December 18, 2020

3. The Wall Street Journal, December 18, 2020

4. CNBC, December 17, 2020

5. The Wall Street Journal, December 16, 2020

6. CNBC, December 16,2020

By: Chris Cook, CPA, CFA

Gilbert & Cook, Chief Investment Strategist

My advice for managing your portfolio in 2021 is a lot like my advice was in 2002 and 2009. And no, I am NOT going to tell you to “stay the course”. I am going to advise that you CHART the course under the calmest of mindset that you can conjure up amid elections and Covid.

Periods of stress change our thinking. Human beings change their mind, second guess, feel regret, and feel blame. So, on a Sunday afternoon, with no screens going and no markets open, set a 10-year course you can stay true to. Balance your 10+ year optimism, (and yes you should have some) with your near-term needs. Two main reasons individual investors fail in times of extreme pessimism as well as extreme optimism is the extrapolation of current events into the future. Things will be bad/good forever. We do not want to be a forced seller or lose our nerve at the bottom of the market in March of 2020. This period of stress, like those before it, has retaught those lessons.

If you have any questions regarding your personal financial situation, please don't hesitate to call a member of our Gilbert & Cook team at 515.270.6444 or email info@gilbertcook.com

The upcoming election is prompting some people to reconsider their investment strategy. But if history is any guide, patience may be the answer.

For the past 12 presidential elections, the Standard & Poor’s 500 index has notched a 4% gain, on average, in the 90 days after the election. (1)

Of course, past performance does not guarantee results. And there have been some notable exceptions to the trend. In 2008, for example, the S&P 500 dropped more than 10% in the three months following the election as the global financial crisis gripped the markets. And in 2000, the S&P 500 fell 4.1% from election day until December 12, when the Supreme Court ruled on the election between George Bush and Al Gore. (1)

Investing involves risks, and your goals, time horizon, and risk tolerance should be what drives any changes to your portfolio strategy. If you’re concerned that the upcoming election may change one of these critical factors, perhaps it's time to review your investment approach.

Regardless of who sits in the white house – business marches to it’s own drummer. Throughout history it has been better to be invested in the optimism of what is going to be created in 5, 10 and 20 years, and not who the president is going to be for the next 4.

In the news and in our social circles we are constantly being told how much we should care about the impact elections are going to have on business . The impact will be there to some extent - sentiment may shift, tax policy may shift, trade policy may shift. But in the long run US ingenuity, entrepreneurship, and the sheer force of creative people getting up and going to work everyday, that’s what’s going to push us forward.

Now is a good time to reflect on a quote from legendary investor Warren Buffett, who reminds us, “The stock market is a device for transferring money from the impatient to the patient.”

Citations

1. HartfordFunds, 2020

TWO FACTORS LEADING TO A RECOVERY

1) Governmental Decisions.

2) Consumer Behavior.

In case you missed it! Here's a clip from our recent virtual event: Elections, Trade and Economy - in our "New Normal". Nationally acclaimed economist, Dr. Chris Kuehl discusses the lasting impact to our current recession and the 2 Factors leading to a recovery.

Gilbert & Cook was announced as one of the top two “Growers Across America” in October 2021, October 2022 and October 2023. CityWire RIA identifies and selects the fastest growing RIAs in each state by analyzing Form ADV data reported to the Securities and Exchange Commission at the time of publication. Data for this publication is gathered by Discovery Data. No compensation was paid in exchange for inclusion in the “50 Growers Across America”.

The Financial Times 300 Top Registered Investment Advisers is an independent listing produced annually by Ignites Research, a division of Money-Media, Inc., on behalf of the Financial Times (July 2020). Areas of consideration include a 3-year growth rate (2016-19) asset assets under management, the company’s age, industry certifications of key employees, SEC compliance record and online accessibility. Neither the RIA firms nor their employees pay a fee to The Financial Times in exchange for inclusion in the FT 300.

To identify the “Best Practices Award” winners, InvestmentNews Research created composite scores which examined rate of growth, profitability, and productivity levels from 2018 to 2019 for all the participants in the InvestmentNews Financial Performance Study. Final firms were selected and awarded in November 2019. Gilbert & Cook did not pay a fee to participate or to receive recognition on this list.